The Stakes: Long-Term Economic Resilience

For two decades, Beijing has pledged to rebalance China’s economy toward household consumption, yet exports and investment remain the dominant drivers of growth. Despite real consumer spending growing at 9% annually — well above the 2% rate in the United States — consumption’s share of gross domestic product (GDP) reached only 41% in 2023, far below the United States’ 69%. The reason is that Beijing has prioritized industrialization, with investment surging from 28% of GDP in 2001 to a peak of 44% in 2014; currently, it stands at 40%.

Slumping investment returns, mounting bad debt, and escalating trade tensions have pushed Beijing to renew its efforts to pivot toward consumption. The fundamental question is not whether consumption-led growth is economically desirable or a priority for China’s leadership, but whether Beijing possesses the political resolve to accept the 2%–3% annual GDP growth that genuine rebalancing would require.

This question sits at the heart of China’s economic future, and it has profound global implications. Since September 2024’s Politburo meeting, Beijing has fundamentally shifted its understanding of consumption’s strategic importance.

Beijing’s pivot represents more than short-term GDP support; it reflects a recognition that consumption is essential for long-term economic resilience and national security. A recent Qiushi essay from the National Development and Reform Commission made this explicit: Strong consumer demand is now essential to national security.

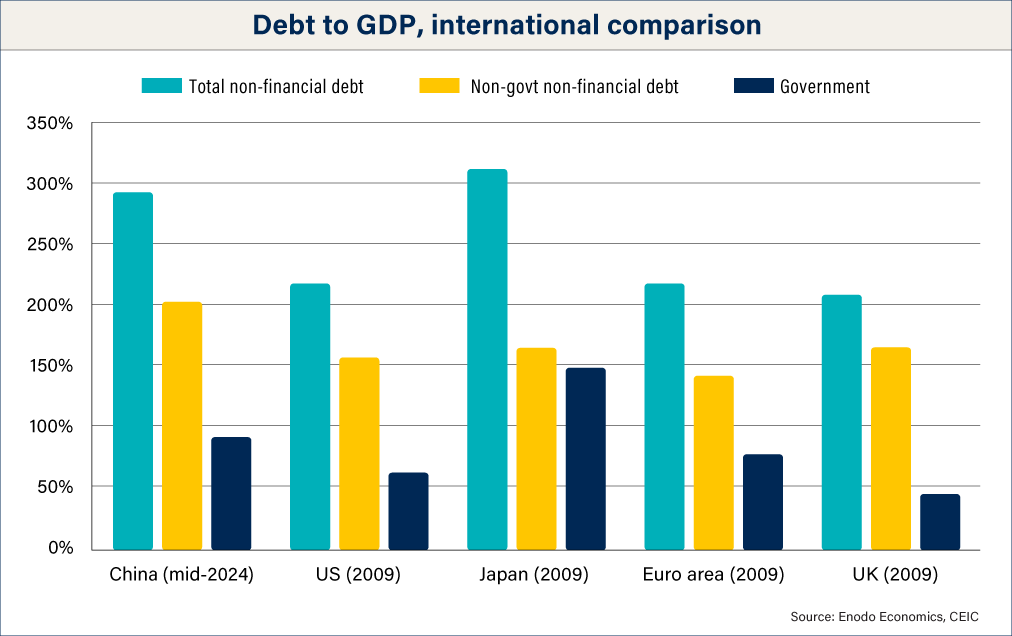

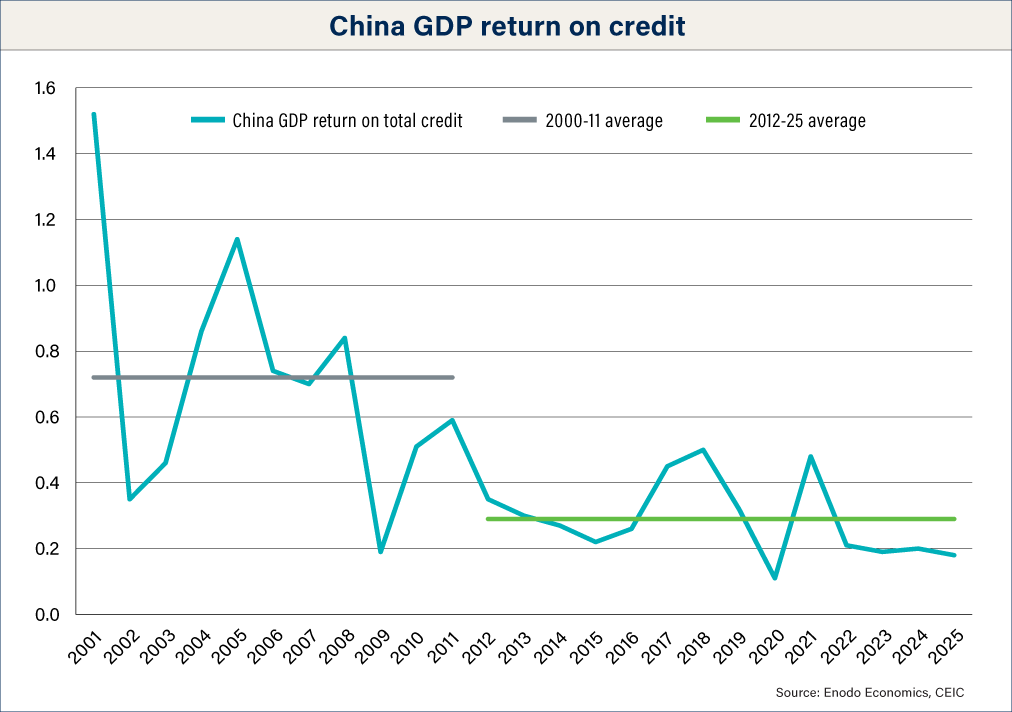

The essay argued that robust domestic markets and internal self-sufficiency are necessary to maintain social stability under “extreme circumstances.” Consumption is now framed as a pillar of economic development and national security. Internationally, escalating trade tensions have reinforced that domestic demand must become the economy’s foundation. China’s nonfinancial debt has surged to 292% of GDP, while returns on nonfinancial, nongovernment credit have been halved, declining to 0.3%. Manufacturing overcapacity has triggered defensive responses worldwide, from U.S. tariffs to European Union investigations.

These deteriorating fundamentals create a political imperative: Without genuine consumer-led growth, social stability becomes increasingly difficult to maintain. China’s leadership can no longer rely on industrial policy and investment to deliver the output and income growth needed to ensure its political legitimacy.

The year 2026 marks the beginning of China’s 15th Five-Year Plan, when Beijing’s consumption strategy will be either institutionalized or abandoned. The Fourth Plenum’s communiqué and subsequent speeches have marked the clearest signal yet that Beijing has moved consumption-led growth from aspiration to a strategic imperative. Whether Beijing can sustain this commitment will determine China’s economic trajectory and global market impact for years to come.

Core Dilemma: Can Beijing Commit to a New Growth Model?

Beijing faces a fundamental contradiction between recognizing that consumption-led growth is essential for survival and maintaining its commitment to state-led technological supremacy. This tension goes beyond policy preferences. Pursuing consumption-led growth requires the state to give up control in key areas: redirecting income and wealth from local governments and state-owned firms to households; allowing individuals to determine their own spending priorities, potentially away from government-prioritized sectors; ending the financial repression of households by letting markets determine the cost of capital; and relying on the private sector to drive innovation.

Meanwhile, continuing to direct domestic savings — currently at artificially low rates — toward investments in chosen technological priorities risks even greater capital misallocation at a time when China has already exhausted the capacity for it, having pursued this model far longer than Japan or Korea ever did.

The scale of rebalancing makes this particularly challenging. Genuine rebalancing would mean households’ income share rising from 61% of GDP to nearly 70%, a redistribution that would necessarily come at the expense of government revenues and state enterprise profits, which currently fund technological ambitions. Local governments would need to shift from infrastructure investment to social transfers, while state-owned enterprises would face pressure to pay higher dividends to households rather than reinvest in industrial capacity.

Equally difficult is the required ideological shift. Xi Jinping’s governance philosophy emphasizes Communist Party control and national security through state dominance of strategic sectors. Consumption-led growth demands the opposite: trusting market mechanisms, expanding space for private entrepreneurs, and allowing household preferences greater influence over resource allocation.

The timing makes this contradiction acute. Just as economic fundamentals are forcing Beijing to embrace consumption-led growth, geopolitical competition is intensifying the drive toward technological self-reliance. The leadership cannot easily explain to its people and its constituents why China should accept slower growth and reduced state control when facing what Beijing frames as an existential technological contest.

Outlook for 2026

The elevation of consumer demand as a priority has been reflected in policy documents since late 2024. December’s Central Economic Work Conference placed boosting household consumption at the top of the agenda. The March 2025 Special Action Plan on Consumption laid out the leadership’s priorities — from income support and burden reduction to optimizing the consumption environment.

The October 2025 Fourth Party Plenum further institutionalized this commitment, with consumption-led growth formally incorporated into the draft 15th Five-Year Plan framework. The Plenum’s work report emphasized that “new demand will lead new supply, and new supply will create new demand,” signaling that household demand expansion would serve as a core pillar of China’s economic strategy through 2030.

While the strategic intent is clear, Beijing’s chosen policy path is suboptimal, and implementation remains gradual. China’s approach to stimulating consumption remains shaped by supply-side logic. Even trade-in subsidy programs are industrial policy in disguise — aimed at upgrading production rather than unleashing household demand, producing only temporary boosts.

Beijing’s resolve remains untested by sustained economic pressure. If the leadership can stay the course through the next five years, consumption’s share of real GDP will grow at a much faster pace than it did during 2010–2019, but with annual GDP growth constrained to 2%–3% at best. Therefore, 2026 will be a crucial test of whether political commitment to structural rebalancing can withstand growth target pressures.15

The most likely outcome is gradual progress under constant pressure. Beijing will continue its pro-consumption rhetoric and incremental measures, but it will likely waver when quarterly growth consistently drops below 3%. The leadership will face intense internal pressure to restore investment-led stimulus, particularly from local governments desperate for fiscal relief and from state-owned enterprises protecting their resource allocation.

This partial commitment is likely to produce some progress on rebalancing — consumption’s share of GDP may rise from 41% to 46%–48% over five years — but fall short of the accelerated transition that economic fundamentals demand. The result will be sustained policy uncertainty as Beijing oscillates between consumption-focused measures and growth-seeking investment, creating volatility and confusion about China’s longer-term economic direction.

Conditions and Contingencies

Beijing’s consumption strategy operates on three fronts: boosting household income, redistributing income toward higher-spending households, and lowering the household savings rate. While conceptually sound, this approach avoids the most effective tools, settling for second-best solutions that will, in the most optimistic scenario, only deliver gradual rather than transformational results.

The Asset Income Challenge

The critical constraint on Chinese consumption is not wage income — China’s wage share of GDP matches that of the United States — but household asset income. Chinese households are large net savers, yet they earn artificially low returns because of financial repression. The optimal solution would involve higher deposit rates, as the bulk of households’ financial wealth is in interest-bearing deposits. Central government debt would need to rise to smooth the necessary adjustments in the state-owned sector, the main beneficiary of artificially low bank rates. This unorthodox approach, however, finds no support among Chinese policymakers.

Instead, Beijing pursues second-best alternatives: redirecting household wealth from property into equity markets through professionalization and higher dividend requirements, and developing rental markets by increasing low-cost rental supply. Rather than allowing markets to set rental prices, the government uses policy measures to manage affordability — again avoiding the direct price mechanism.

These reforms show promise but require time. The equity market expansion could meaningfully boost household asset income if it is accompanied by genuine corporate governance improvements and dividend policies. The rental market development will provide real income gains by reducing housing-cost burdens, particularly for younger urban households.

Redistribution and Its Limitations

The second prong involves redistributing income from households with low marginal propensity to consume to those with high marginal propensity to consume, through expanded social transfers such as housing and education cost support and rural support programs. Although this approach is theoretically sound, it faces practical uncertainties. The spending propensities of different income groups may not align with expectations, and absolute spending increases among beneficiaries may not offset spending reductions among those facing higher taxes or reduced income.

Healthcare costs, education expenses, eldercare burdens, and inadequate social security also underpin China’s excessively high savings rate. Boosting social security transfers helps lower households’ desire to save too much of their income. But this measure is likely to be less potent than addressing the decades-long household financial repression — the low return on household wealth leading to excessive precautionary savings.

The Missing Piece: Ending Financial Repression

The most potent and likely the fastest-acting tool — ending household financial repression through higher interest rates — remains off the table. Without market-determined returns on savings, households will continue to save excessively and seek alternative stores of value, whether in property, overseas assets, or other nonproductive channels.

Beijing’s strategy will likely generate measurable progress over the next five years, particularly through equity and rental market development. However, refusing to address financial repression directly means that consumption gains will remain gradual and incomplete, requiring extended time frames and increasing the likelihood of relapses toward growth led by investment and/or exports instead.

What to Watch

Determining whether Beijing can sustain its consumption-led pivot requires monitoring key indicators that will reveal both policy commitment and underlying economic pressures:

Maintaining consumption policies despite growth pressure in order to signal authentic resolve.

Integration of consumption metrics into local government performance evaluations and five-year plan targets.

Financial market reforms to end household financial repression, allowing higher deposit rates and expanding household investment options.

Return to investment-led stimulus during GDP growth slowdowns, such as large infrastructure packages or property market easing.

Local governments prioritizing infrastructure over social transfers when facing budget constraints.

Household asset income trajectory relative to GDP from equity market development and dividend policies.

Broad-based consumption growth rather than consumption focused solely on subsidy-dependent categories like electric vehicles.

Consumption growth without excessive household debt accumulation.

Alternative Scenarios

Baseline (most likely): Gradual progress under pressure. Beijing maintains its consumption rhetoric but wavers when growth drops below 3%. Incremental measures, such as social transfers and modest equity reforms, result in an increase in consumption’s share of GDP from 41% to 46%–48% in the next five years. However, policy oscillation between consumption support and investment stimulus creates market uncertainty while achieving insufficient structural change.

Alternative 1: Resolute structural transition. Leadership accepts 2%–3% GDP growth as the price of genuine rebalancing. Consumption metrics become institutionalized in performance evaluations, equity market development meaningfully boosts household asset income, and consumption’s share of GDP reaches 50%–55% by the end of the 15th Five-Year Plan. This scenario requires exceptional political discipline to maintain the course.

Alternative 2 (least likely): Growth target capitulation. Political pressure forces Beijing to abandon the consumption strategy as GDP approaches 2%. We see a return to investment-led stimulus, property easing, and export promotion as Beijing tries to restore traditional growth rates. The attempt to postpone structural problems most likely fails.

Strategic Implications

Domestically, the baseline scenario creates extended economic volatility as policy oscillation between consumption and investment priorities generates uncertainty. Partial reforms prolong adjustment pain, and rebalancing benefits accrue slowly.

Alternatively, resolute structural transition produces a more sustainable economic model with slower GDP growth. Household-income and welfare improvements provide alternative sources of legitimacy, while equity market development creates new wealth-building opportunities.

In the area of U.S.-China relations, successful consumption rebalancing reduces bilateral goods trade surpluses and some trade tensions while maintaining strategic technological rivalry. The baseline scenario perpetuates trade conflicts amid policy uncertainty. Alternatively, growth target capitulation triggers the most severe trade wars as China pursues desperate export-led growth through currency manipulation and subsidies.

On the global stage, genuine Chinese consumption growth creates significant opportunities for export-driven economies, particularly in consumer goods and services. The baseline scenario generates market uncertainty as companies navigate unpredictable Chinese demand cycles. Chinese capitulation destabilizes global markets through export flooding and potential financial contagion, particularly pressuring emerging markets.

Policy Shaping and Conclusion

China’s shift toward a consumption-led growth model will require not only the right policy design but also political endurance. Sustained rebalancing calls for structural redistribution from the state sector to households, a relaxation of financial repression, and acceptance of lower headline growth in exchange for greater economic resilience. The central question is whether Beijing can institutionalize these priorities and maintain its commitment to them when short-term growth pressures mount.

To succeed, China should embed consumption metrics within local and national performance frameworks, and develop institutional safeguards that preserve pro-consumption policies through cyclical downturns. Redefining policy success around household prosperity, rather than aggregate GDP, would strengthen legitimacy and social stability. The most impactful reform — ending household financial repression through higher deposit rates and improved capital market access — remains essential to unlocking sustained consumption gains.

For the United States and global partners, strategic engagement should encourage China’s domestic rebalancing while preparing for volatility if reforms stall. Coordinated contingency planning for potential export surges and diversified demand channels will be critical. The durability of China’s consumption pivot will shape both its own internal equilibrium and global economic stability.